Update (1015ET): French credit risk surged after Le Pen's opposition party National Rally confirmed it will back a no-confidence motion brought by the Left's Manot (who confirmed he will do so on national TV), after PM Barnier used article 49.3 to push through a spending bill that crossed too many red lines.

“There is no way out for a government that reconnects with the thread of Macronism, which refuses to take into account the social emergency at the end of the month and which ignores the need to relaunch growth,” National Rally President Jordan Bardella wrote on X after the announcement.

"We will vote no confidence," the RN said on X.

Le Pen's RN party is the largest single party in parliament.

The left wing is also expected to back the motion, which could be held as early as Wednesday and if successful would topple the minority government after only three months in office.

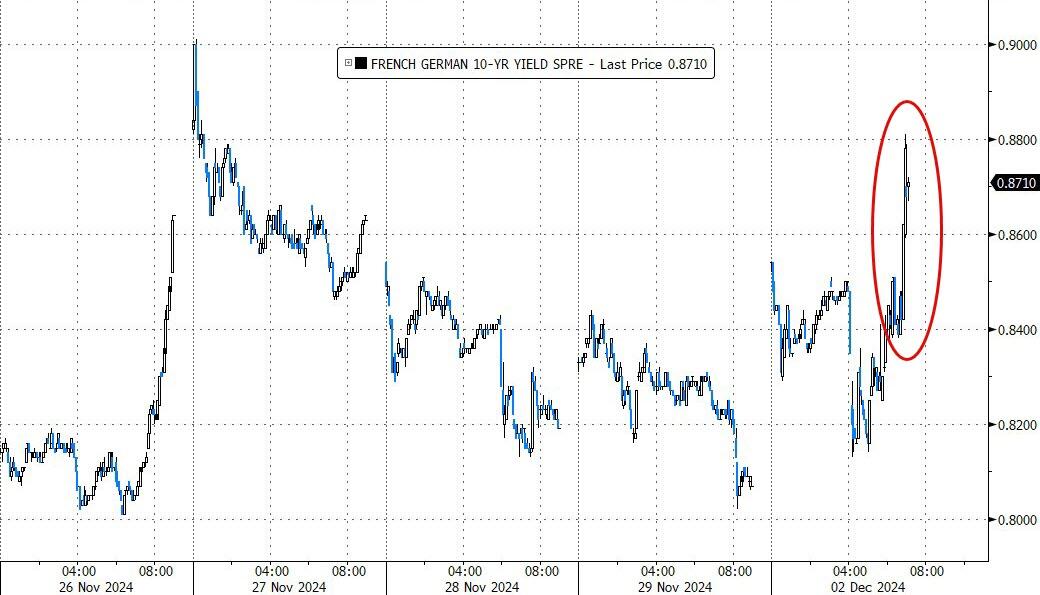

French credit spread (to Germany) snapped higher on the news (even though it was expected)

French shares are also tumbling as the country's yields are now higher than Greece's...

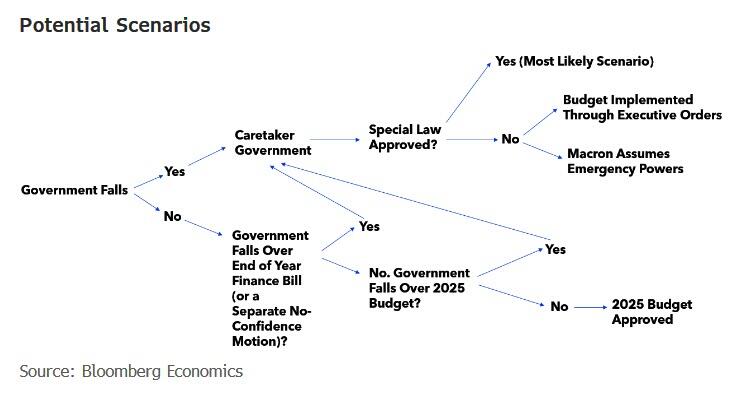

If Barnier is evicted from office, Macron would have to re-appoint him or pick a new premier.

But the president would face the same difficult balancing act with no possibility for fresh legislative elections until July.

Any new government that emerges would still need urgently to propose a 2025 budget.

* * *

France’s benchmark yield spreads have come off the day’s wides after the latest headlines show the government may have made a further compromise in its bid to save the budget.

France’s government offered a final-hour concession to Marine Le Pen on the 2025 budget, seeking to avoid being ousted from power in a no-confidence vote.

Prime Minister Michel Barnier committed to not cutting reimbursements for medicines, caving to yet another key demand from the far-right after crisis talks with Le Pen earlier Monday.

The concession is a last-ditch attempt by the French premier to keep the budget bill on track and remain in office. Without a majority in parliament, Barnier was set to resort to using Article 49.3, which allows for the adoption of the social security bill without a vote, but opens the door to no-confidence motions.

Le Pen’s National Rally party, the largest in the lower house, said earlier Monday it would ensure the government falls, barring a “miracle” compromise on their demands. Party officials did not immediately respond to requests for comment after Barnier offered the concession.

However, at 83bps (spread to Bunds), French fragmentation risk remains as high as it has been since the EU financial crisis in 2013 ahead of the critical vote...

Source: Bloomberg

How Did We Get Here...?

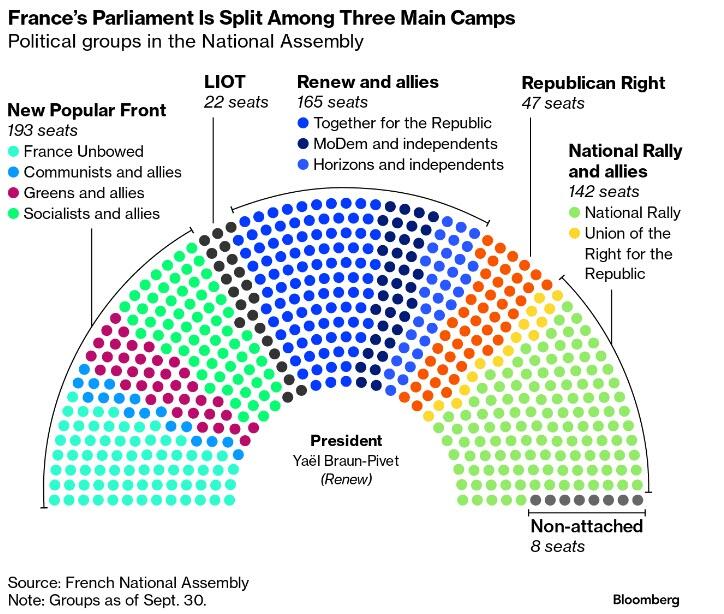

Before the end of today's French parliamentary session, Barnier's government must submit the social security budget details to the National Assembly. As it stands, Barnier's center-right gov't cannot pass this unless National Rally (RN) provides support or abstains. Currently. Barnier's coalition has the most seats followed by New Popular Front (NFP) and then RN.

Barnier has already made clear he plans to pass the motion via Article 49.3, which allows the gov't to pass measures without a formal parliamentary vote but at the cost of opening the door to an immediate no-confidence motion.

In recent days Barnier made concessions to RN’s Le Pen around electricity taxes and certain other issues in order to get her support and avoid losing the no-confidence motion. However, Le Pen has made clear that RN has multiple red lines which need to be removed from the budget.

On Sunday, Le Pen announced that Barnier had ended the discussion' while more recently RN’s Bardella said "a no-confidence motion will likely be passed unless there is a last minute miracle”.

Ratings

S&P affirmed France at AA- on Friday, with a Stable outlook, recognizing Barnier's austerity plan to reduce the deficit. However, the agency warned that political fragmentation and the risk of diluted reforms could threaten long-term fiscal stability, and while it is optimistic about 2025's fiscal targets, it cautioned that the future trajectory beyond 2025 remains uncertain.

What Happens Next?

On Monday, 2nd December Barnier's gov't will announce they are passing the social security budget via Article 49.3. After which, opposition parties will be entitled to table a no-confidence motion.

The left-wing alliance NFP is expected to table such a motion. As a reminder. NFP secured the most seats in June's election but President Macron decided not to select the PM from that group and instead tried to form a centrist coalition with Barnier at its helm. As such, they have committed to tabling a no-confidence motion which will pass if, and only if. RN supports it.

If tabled, the motion will likely occur on Wednesday, 4th December. After Article 49.3 is used opposition parties have up to 48-hours to table a no-confidence motion which then needs to be voted on within three days. However, there is no reason for NFP not to table the motion immediately, hence Wednesday is the most likely day. For what it's worth. RN also appears to have a no-confidence motion ready to go.

Following this, the next step goes to President Macron who will attempt to appoint a new PM. get support around them and then pass the required fiscal legislation by year end to have a workable budget for 2025 and appease the European Commission. As a reminder, the Commission placed France under excessive deficit procedures due to its deficit being well in excess of the 3% debt/GDP ratio the commission allows.

In the event that Barnier survives the confidence motion then he has to return before end-December with the management component of the budget.

A bill which would also need Article 49.3 to pass and thus will open the door to another confidence motion.

If Barnier loses the motion then Macron will need to appoint someone to serve as the new PM.

In the short-term, Barnier would likely continue as a caretaker during which there are two backup options for the government: 1) usage of special legislation to rollover the 2024 budget for a brief period of time (this would not solve the pressing budget problems); 2) usage of a gov't order to pass the budget without vote, while this would pass the budget there would be no gov't to deliver it (Barnier couldn't as caretaker), thus Macron would need to appoint a new PM.

A government which would undoubtedly face even greater pressure from NFP and RN.

Le Pen

It is somewhat unclear as to what exactly Le Pen wishes to gain from the gov't collapsing.

As parliament cannot be dissolved until June 2025 at the earliest and while the gov't collapsing will put pressure on Macron to resign, he has made clear he will not do so.

There had been speculation that Le Pen’s stance was a negotiating tactic in order to obtain some of her red lines. If this is the case, then it is going to the wire.

Finally, the impact of this is not inconsequential...

It has historically cost the French government around 50bps more to finance itself for 10 years than it has the German government. France is now the euro-area’s biggest issuer of debt (ahead of Italy) and the country ran a huge budget deficit in 2024. The political turmoil created since Macron called a snap parliamentary election has seen that spread widen to around 85 bps.

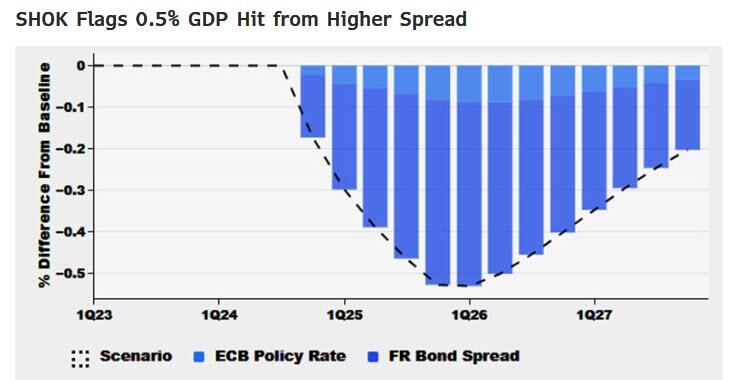

Running the wider spread through our in-house model of the euro-area economies, and assuming it remains elevated through 2025, suggests a 0.5% drag on GDP will emerge by the end of next year.

Higher borrowing costs and slower growth would be a bad combination for public finances. The danger is that spreads widen further, exacerbating these impacts and creating ever bigger fiscal risks.

Update (1015ET): French credit risk surged after Le Pen's opposition party National Rally confirmed it will back a no-confidence motion brought by the Left's Manot (who confirmed he will do so on national TV), after PM Barnier used article 49.3 to push through a spending bill that crossed too many red lines.

“There is no way out for a government that reconnects with the thread of Macronism, which refuses to take into account the social emergency at the end of the month and which ignores the need to relaunch growth,” National Rally President Jordan Bardella wrote on X after the announcement.

"We will vote no confidence," the RN said on X.

Le Pen's RN party is the largest single party in parliament.

The left wing is also expected to back the motion, which could be held as early as Wednesday and if successful would topple the minority government after only three months in office.

French credit spread (to Germany) snapped higher on the news (even though it was expected)

French shares are also tumbling as the country's yields are now higher than Greece's...

If Barnier is evicted from office, Macron would have to re-appoint him or pick a new premier.

But the president would face the same difficult balancing act with no possibility for fresh legislative elections until July.

Any new government that emerges would still need urgently to propose a 2025 budget.

* * *

France’s benchmark yield spreads have come off the day’s wides after the latest headlines show the government may have made a further compromise in its bid to save the budget.

France’s government offered a final-hour concession to Marine Le Pen on the 2025 budget, seeking to avoid being ousted from power in a no-confidence vote.

Prime Minister Michel Barnier committed to not cutting reimbursements for medicines, caving to yet another key demand from the far-right after crisis talks with Le Pen earlier Monday.

The concession is a last-ditch attempt by the French premier to keep the budget bill on track and remain in office. Without a majority in parliament, Barnier was set to resort to using Article 49.3, which allows for the adoption of the social security bill without a vote, but opens the door to no-confidence motions.

Le Pen’s National Rally party, the largest in the lower house, said earlier Monday it would ensure the government falls, barring a “miracle” compromise on their demands. Party officials did not immediately respond to requests for comment after Barnier offered the concession.

However, at 83bps (spread to Bunds), French fragmentation risk remains as high as it has been since the EU financial crisis in 2013 ahead of the critical vote...

Source: Bloomberg

How Did We Get Here...?

Before the end of today's French parliamentary session, Barnier's government must submit the social security budget details to the National Assembly. As it stands, Barnier's center-right gov't cannot pass this unless National Rally (RN) provides support or abstains. Currently. Barnier's coalition has the most seats followed by New Popular Front (NFP) and then RN.

Barnier has already made clear he plans to pass the motion via Article 49.3, which allows the gov't to pass measures without a formal parliamentary vote but at the cost of opening the door to an immediate no-confidence motion.

In recent days Barnier made concessions to RN’s Le Pen around electricity taxes and certain other issues in order to get her support and avoid losing the no-confidence motion. However, Le Pen has made clear that RN has multiple red lines which need to be removed from the budget.

On Sunday, Le Pen announced that Barnier had ended the discussion' while more recently RN’s Bardella said "a no-confidence motion will likely be passed unless there is a last minute miracle”.

Ratings

S&P affirmed France at AA- on Friday, with a Stable outlook, recognizing Barnier's austerity plan to reduce the deficit. However, the agency warned that political fragmentation and the risk of diluted reforms could threaten long-term fiscal stability, and while it is optimistic about 2025's fiscal targets, it cautioned that the future trajectory beyond 2025 remains uncertain.

What Happens Next?

On Monday, 2nd December Barnier's gov't will announce they are passing the social security budget via Article 49.3. After which, opposition parties will be entitled to table a no-confidence motion.

The left-wing alliance NFP is expected to table such a motion. As a reminder. NFP secured the most seats in June's election but President Macron decided not to select the PM from that group and instead tried to form a centrist coalition with Barnier at its helm. As such, they have committed to tabling a no-confidence motion which will pass if, and only if. RN supports it.

If tabled, the motion will likely occur on Wednesday, 4th December. After Article 49.3 is used opposition parties have up to 48-hours to table a no-confidence motion which then needs to be voted on within three days. However, there is no reason for NFP not to table the motion immediately, hence Wednesday is the most likely day. For what it's worth. RN also appears to have a no-confidence motion ready to go.

Following this, the next step goes to President Macron who will attempt to appoint a new PM. get support around them and then pass the required fiscal legislation by year end to have a workable budget for 2025 and appease the European Commission. As a reminder, the Commission placed France under excessive deficit procedures due to its deficit being well in excess of the 3% debt/GDP ratio the commission allows.

In the event that Barnier survives the confidence motion then he has to return before end-December with the management component of the budget.

A bill which would also need Article 49.3 to pass and thus will open the door to another confidence motion.

If Barnier loses the motion then Macron will need to appoint someone to serve as the new PM.

In the short-term, Barnier would likely continue as a caretaker during which there are two backup options for the government: 1) usage of special legislation to rollover the 2024 budget for a brief period of time (this would not solve the pressing budget problems); 2) usage of a gov't order to pass the budget without vote, while this would pass the budget there would be no gov't to deliver it (Barnier couldn't as caretaker), thus Macron would need to appoint a new PM.

A government which would undoubtedly face even greater pressure from NFP and RN.

Le Pen

It is somewhat unclear as to what exactly Le Pen wishes to gain from the gov't collapsing.

As parliament cannot be dissolved until June 2025 at the earliest and while the gov't collapsing will put pressure on Macron to resign, he has made clear he will not do so.

There had been speculation that Le Pen’s stance was a negotiating tactic in order to obtain some of her red lines. If this is the case, then it is going to the wire.

Finally, the impact of this is not inconsequential...

It has historically cost the French government around 50bps more to finance itself for 10 years than it has the German government. France is now the euro-area’s biggest issuer of debt (ahead of Italy) and the country ran a huge budget deficit in 2024. The political turmoil created since Macron called a snap parliamentary election has seen that spread widen to around 85 bps.

Running the wider spread through our in-house model of the euro-area economies, and assuming it remains elevated through 2025, suggests a 0.5% drag on GDP will emerge by the end of next year.

Higher borrowing costs and slower growth would be a bad combination for public finances. The danger is that spreads widen further, exacerbating these impacts and creating ever bigger fiscal risks.