By Michael Every of Rabobank

When the Fed cut rates by ‘only-in-an-emergency’ 50bps on September 18 as it Orwell-style said the US economy was “good”, I wonder if their army of market economists had warned them that just over a month later, the 2- and 10-year US Treasury yield would both be trading around 50bps higher at 4.02% and 4.18% - and with market chatter that we could test 5% in the latter ahead?

If they did, why did the Fed cut when they wanted to see lower yields? If they didn’t, does the Fed know what they are doing? Consider that as the Fed’s Daly says she doesn’t see any reason not to continue cutting rates as inflation falls (and yields rise?) to guard against further weakening of the labor market (which isn’t being shown in the latest data). Other voices are at least suggesting the next steps might be back to 25bps (which might see yields rise relatively less?), and Kashkari is again asking out loud if the neutral US rate might now be higher.

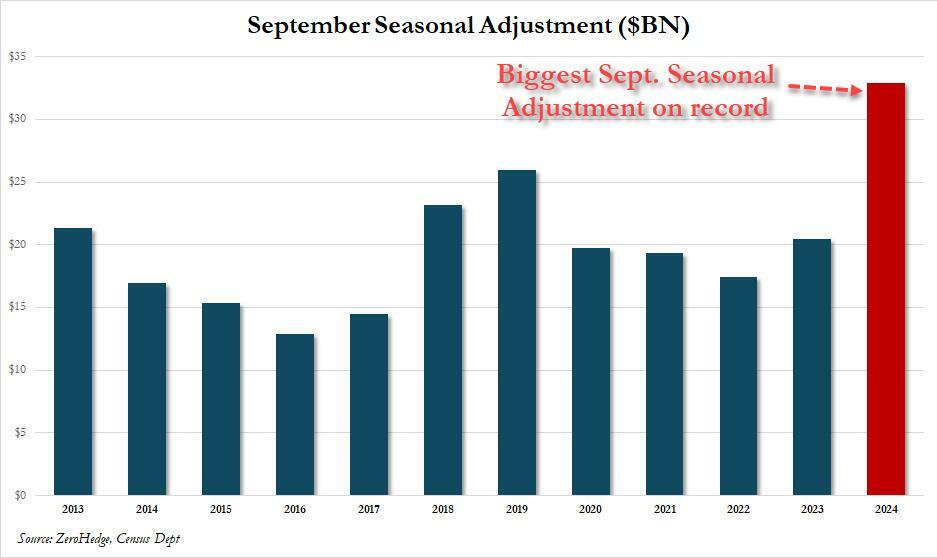

Of course, some of the (very) seasonally adjusted US data of late explains part of that yield pop. However, so might the US election now two weeks away as betting markets - whatever they are worth - increasingly back Trump to win: are are seeing Trump trades related to higher inflation(?)

There’s certainly no lack of election hyperbole. Vanity Fair warns, “We All Have a Lot to Lose If Trump Wins”, as “A second Trump presidency could mark the end of something we certainly don’t want to lose: democracy as we know it.” The Atlantic says, ‘Trump Is Speaking Like Hitler, Stalin, and Mussolini’ – did they do rude jokes about golfers? Rolling Stone opts for ‘Trump’s Closing Pitch to Voters: I Will Let You Die If You Don’t Bow to My Demands’. This is the mainstream media.

Yet the financial market focus seems far more particular: on trade and tariffs. Bloomberg - in the non-partisan manner expected from a financial news organization whose billionaire owner ran for president against Trump in 2020 - editorialises that, ‘Harris Should Challenge Trump on Trade and Tariffs’. Yet their analysis on tariffs is awful. They link to another story, ‘Two US Towns Show What Happens When China Gets Hit With Tariffs’, as evidence of why tariffs don’t work and Biden is as flawed as Trump in seeing trade as zero sum. Except that the logic of the article fails to make that point at all.

It underlines that Biden tariffs on trailers used to tow 40’ shipping containers saw a Chinese firm set up production in the US – which backs tariffs; the rival US firm was found to be using Chinese steel ostensibly coming from Thailand, so also got hit with duties – which backs tariffs shifting supply chains globally, over time; the Chinese firm was alleged to be using Chinese steel ostensibly from Vietnam – which makes the same point; and the story concludes that the industry was hit hard by the end of Covid lockdown and a sharp reduction in the need for trailers as port activity normalised – which has NOTHING TO DO WITH TARIFFS. Nonetheless, it is apparently important to Bloomberg that Harris distance herself from Biden’s and Trump’s trade wars and start to shift towards free trade, as if this were a vote winner. It might be in the Bloomberg building given financial news media naturally prefer the US to export financial assets such as Treasury bonds rather than physical goods such as trailers; but polls don’t suggest Main Street echoes that.

I’m not saying tariffs can’t be inflationary: they can and likely will be – and that’s our base case ahead. But if the above is ‘analysis’ of all the economic, political, and geopolitical dimensions of this complex issue, then I suggest the authors might want to apply for a job in the economics department at the Fed.

Staying with bad analysis, as the market loses focus on the Middle East, the news is far from good. Israeli reports suggest the recent Hezbollah drone strike on PM Netanyahu’s house will prompt a more severe retaliatory hit on Iran than previously planned. While the logistics of the original scheme were leaked to Iran by the US, which scuppered an Israeli attack on Iran’s nuclear program when it also happened in 2012, this time it adds to the Israeli argument to up the military ante and not tell the US what it’s going to do in advance. Rumors are of strikes on Iranian leaders’ homes as well as military, economic, and nuclear sites – and the expectation is of a strong response leading to escalation… until oil is eventually hit? Tellingly, in Lebanon, Israel is striking a Hezbollah-linked bank to cripple it financially; and released a video informing the Lebanese that Hezbollah has $500m in cash and gold in a bunker underneath a Beirut hospital, which it won’t strike (with the implication people should go help themselves). If that approach is carried over to Iran, markets may get a short, sharp shock.

IDF just went It's a Mad, Mad, Mad, Mad World on Lebanon and told everyone where Hezbollah's millions of dollars in cash and gold are hidden. 🤣 pic.twitter.com/rdr0O0yvUv

— The Mossad: Satirical and Awesome (@TheMossadIL) October 21, 2024

No analysis is also bad analysis. Tiny Moldova just voted to start the EU accession process with a 50.39% vs. 49.61% referendum victory: given its small population, only 11,602 votes decided the country’s future. Regardless, Moldova, with a GDP per capita of just $6,651, and bordering the breakaway pro-Russian region of Transnistria, now starts the slow process towards joining the EU (and the Euro?). Expect EU-Russia tensions to continue to grow as a result. Moreover, the ever cheery but always readable Branko Milanovic notes, “For small countries that are polarized in many respects, it is a suicide in this geo-political climate, to choose one or the other side. Neutrality or non-alignment is not just a "nice" policy. It is necessary in order to survive without a civil war. Libya & Iraq are cautionary tales.”

For small countries that are polarized in many respects, it is a suicide in this geo-political climate, to choose one or the other side. Neutrality or non-alignment is not just a "nice" policy. It is necessary in order to survive without a civil war. Libya & Iraq are cautionary…

— Branko Milanovic (@BrankoMilan) October 21, 2024

And today, at the macro level, while Washington, D.C. hosts the annual IMF and World Bank meetings “clouded by war, slow economic growth, and the US election” - where we can expect much muttering about tariffs - we also get the BRICS summit in Kazan, Russia, the first since the group expanded, to far less Western attention.

While there is no chance of a BRICS FX alternative to the US dollar emerging, we might see progress towards Russia’s plans for a BRICS exchange for producers and consumers of almost half of global grains – or ‘BREAD-PEC’. While pricing of these commodities will surely remain in dollars, mechanisms may be proposed for price floors and ceilings; moreover, we may also see increased institutional BRICS barter to obviate the need to transact grains trade in dollars. With major grain producers such as the US, Canada, Australia, the EU, and Ukraine not involved, the embryonic outlines of a potential global bifurcation in key agri markets may be there. (As Russia bans imports of Kazakh grains, fruits, and vegetables for ‘failing phytosanitary standards’ following the country’s decision not to join the BRICS.)

Moreover, if this grains exchange works, which is far from certain, expect attempts to roll it out to other commodities the BRICS are rich in. Even so, those thinking we will get to the same outcome in energy any time soon are failing to do serious analysis of their own; if not, those looking at US bond yields really are.

By Michael Every of Rabobank

When the Fed cut rates by ‘only-in-an-emergency’ 50bps on September 18 as it Orwell-style said the US economy was “good”, I wonder if their army of market economists had warned them that just over a month later, the 2- and 10-year US Treasury yield would both be trading around 50bps higher at 4.02% and 4.18% - and with market chatter that we could test 5% in the latter ahead?

If they did, why did the Fed cut when they wanted to see lower yields? If they didn’t, does the Fed know what they are doing? Consider that as the Fed’s Daly says she doesn’t see any reason not to continue cutting rates as inflation falls (and yields rise?) to guard against further weakening of the labor market (which isn’t being shown in the latest data). Other voices are at least suggesting the next steps might be back to 25bps (which might see yields rise relatively less?), and Kashkari is again asking out loud if the neutral US rate might now be higher.

Of course, some of the (very) seasonally adjusted US data of late explains part of that yield pop. However, so might the US election now two weeks away as betting markets - whatever they are worth - increasingly back Trump to win: are are seeing Trump trades related to higher inflation(?)

There’s certainly no lack of election hyperbole. Vanity Fair warns, “We All Have a Lot to Lose If Trump Wins”, as “A second Trump presidency could mark the end of something we certainly don’t want to lose: democracy as we know it.” The Atlantic says, ‘Trump Is Speaking Like Hitler, Stalin, and Mussolini’ – did they do rude jokes about golfers? Rolling Stone opts for ‘Trump’s Closing Pitch to Voters: I Will Let You Die If You Don’t Bow to My Demands’. This is the mainstream media.

Yet the financial market focus seems far more particular: on trade and tariffs. Bloomberg - in the non-partisan manner expected from a financial news organization whose billionaire owner ran for president against Trump in 2020 - editorialises that, ‘Harris Should Challenge Trump on Trade and Tariffs’. Yet their analysis on tariffs is awful. They link to another story, ‘Two US Towns Show What Happens When China Gets Hit With Tariffs’, as evidence of why tariffs don’t work and Biden is as flawed as Trump in seeing trade as zero sum. Except that the logic of the article fails to make that point at all.

It underlines that Biden tariffs on trailers used to tow 40’ shipping containers saw a Chinese firm set up production in the US – which backs tariffs; the rival US firm was found to be using Chinese steel ostensibly coming from Thailand, so also got hit with duties – which backs tariffs shifting supply chains globally, over time; the Chinese firm was alleged to be using Chinese steel ostensibly from Vietnam – which makes the same point; and the story concludes that the industry was hit hard by the end of Covid lockdown and a sharp reduction in the need for trailers as port activity normalised – which has NOTHING TO DO WITH TARIFFS. Nonetheless, it is apparently important to Bloomberg that Harris distance herself from Biden’s and Trump’s trade wars and start to shift towards free trade, as if this were a vote winner. It might be in the Bloomberg building given financial news media naturally prefer the US to export financial assets such as Treasury bonds rather than physical goods such as trailers; but polls don’t suggest Main Street echoes that.

I’m not saying tariffs can’t be inflationary: they can and likely will be – and that’s our base case ahead. But if the above is ‘analysis’ of all the economic, political, and geopolitical dimensions of this complex issue, then I suggest the authors might want to apply for a job in the economics department at the Fed.

Staying with bad analysis, as the market loses focus on the Middle East, the news is far from good. Israeli reports suggest the recent Hezbollah drone strike on PM Netanyahu’s house will prompt a more severe retaliatory hit on Iran than previously planned. While the logistics of the original scheme were leaked to Iran by the US, which scuppered an Israeli attack on Iran’s nuclear program when it also happened in 2012, this time it adds to the Israeli argument to up the military ante and not tell the US what it’s going to do in advance. Rumors are of strikes on Iranian leaders’ homes as well as military, economic, and nuclear sites – and the expectation is of a strong response leading to escalation… until oil is eventually hit? Tellingly, in Lebanon, Israel is striking a Hezbollah-linked bank to cripple it financially; and released a video informing the Lebanese that Hezbollah has $500m in cash and gold in a bunker underneath a Beirut hospital, which it won’t strike (with the implication people should go help themselves). If that approach is carried over to Iran, markets may get a short, sharp shock.

IDF just went It's a Mad, Mad, Mad, Mad World on Lebanon and told everyone where Hezbollah's millions of dollars in cash and gold are hidden. 🤣 pic.twitter.com/rdr0O0yvUv

— The Mossad: Satirical and Awesome (@TheMossadIL) October 21, 2024

No analysis is also bad analysis. Tiny Moldova just voted to start the EU accession process with a 50.39% vs. 49.61% referendum victory: given its small population, only 11,602 votes decided the country’s future. Regardless, Moldova, with a GDP per capita of just $6,651, and bordering the breakaway pro-Russian region of Transnistria, now starts the slow process towards joining the EU (and the Euro?). Expect EU-Russia tensions to continue to grow as a result. Moreover, the ever cheery but always readable Branko Milanovic notes, “For small countries that are polarized in many respects, it is a suicide in this geo-political climate, to choose one or the other side. Neutrality or non-alignment is not just a "nice" policy. It is necessary in order to survive without a civil war. Libya & Iraq are cautionary tales.”

For small countries that are polarized in many respects, it is a suicide in this geo-political climate, to choose one or the other side. Neutrality or non-alignment is not just a "nice" policy. It is necessary in order to survive without a civil war. Libya & Iraq are cautionary…

— Branko Milanovic (@BrankoMilan) October 21, 2024

And today, at the macro level, while Washington, D.C. hosts the annual IMF and World Bank meetings “clouded by war, slow economic growth, and the US election” - where we can expect much muttering about tariffs - we also get the BRICS summit in Kazan, Russia, the first since the group expanded, to far less Western attention.

While there is no chance of a BRICS FX alternative to the US dollar emerging, we might see progress towards Russia’s plans for a BRICS exchange for producers and consumers of almost half of global grains – or ‘BREAD-PEC’. While pricing of these commodities will surely remain in dollars, mechanisms may be proposed for price floors and ceilings; moreover, we may also see increased institutional BRICS barter to obviate the need to transact grains trade in dollars. With major grain producers such as the US, Canada, Australia, the EU, and Ukraine not involved, the embryonic outlines of a potential global bifurcation in key agri markets may be there. (As Russia bans imports of Kazakh grains, fruits, and vegetables for ‘failing phytosanitary standards’ following the country’s decision not to join the BRICS.)

Moreover, if this grains exchange works, which is far from certain, expect attempts to roll it out to other commodities the BRICS are rich in. Even so, those thinking we will get to the same outcome in energy any time soon are failing to do serious analysis of their own; if not, those looking at US bond yields really are.