Fed chair Jerome Powell has signaled that interest rate cuts are on the horizon, amid a cooling labor market marked by fewer job additions and rising unemployment.

Today, the benchmark interest rate stands at 5.25- 5.50%, up from near-zero levels in 2022. Historically, equities have performed better after gradual rate cuts compared to swift reductions typically seen during economic crises. Sectors of the economy are also impacted in different ways, due to shifting consumer demand and interest rate sensitivity.

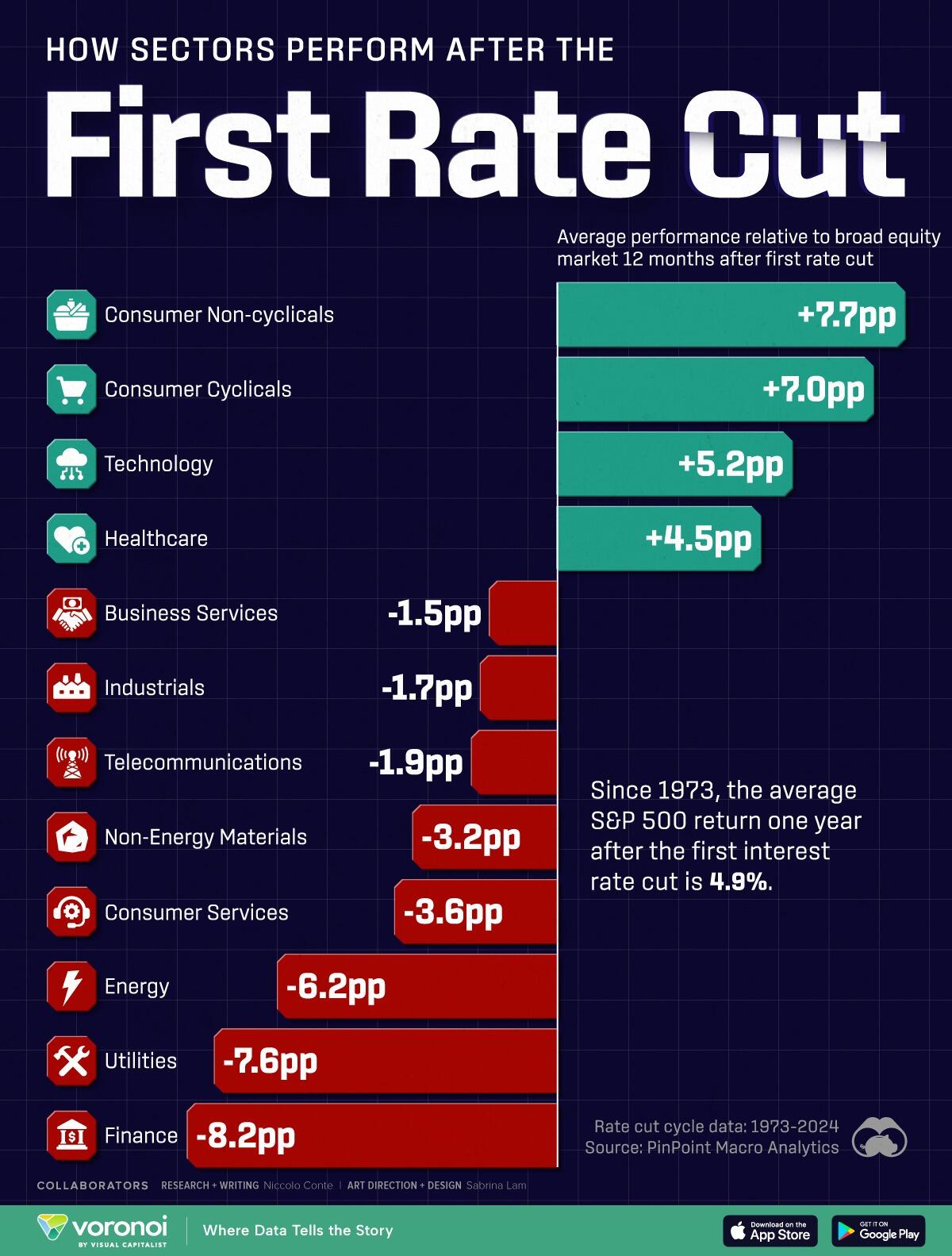

This graphic, via Visual Capitalist's Dorothy Neufeld, breaks down sector performance after the first interest rate cut, based on data from PinPoint Macro Analytics.

Ranked: Sector Performance During Rate Cut Cycles

Below, we show the average performance of each sector relative to the broad equity market 12 months after the first rate cut between 1973 and 2024:

Average historical data of rate cycles from 1973 to present day.

Consumer non-cyclicals see the strongest returns after the first rate cut, particularly during recessions, thanks to steady demand for staple goods.

This traditionally defensive sector includes companies such as Procter & Gamble, Walmart, and Coca-Cola. Notably, consumer staples are the only S&P 500 sector that have produced positive returns on average, during the recession stage of the business cycle since 1960. During the slowdown phase, it also outperformed the vast majority of sectors, averaging 15% returns over these periods.

Meanwhile, the tech sector underperforms the market six months after the first rate cut, but performance bounces back over a 12 month period since lower interest rates generally benefit growth stocks by reducing borrowing costs. However, some of today’s largest tech companies have been more resilient to higher rates due to large cash reserves and heightened investor interest in AI-related stocks.

On the other hand, financials historically experience the weakest performance. This is due to the fact that interest rate cuts often signal that the economy is slowing, putting pressure on loan growth, credit losses, and default risk.

To learn more about this topic from a sector-composition perspective, check out this graphic on the largest company in each S&P 500 sector in 2024.

Fed chair Jerome Powell has signaled that interest rate cuts are on the horizon, amid a cooling labor market marked by fewer job additions and rising unemployment.

Today, the benchmark interest rate stands at 5.25- 5.50%, up from near-zero levels in 2022. Historically, equities have performed better after gradual rate cuts compared to swift reductions typically seen during economic crises. Sectors of the economy are also impacted in different ways, due to shifting consumer demand and interest rate sensitivity.

This graphic, via Visual Capitalist's Dorothy Neufeld, breaks down sector performance after the first interest rate cut, based on data from PinPoint Macro Analytics.

Ranked: Sector Performance During Rate Cut Cycles

Below, we show the average performance of each sector relative to the broad equity market 12 months after the first rate cut between 1973 and 2024:

Average historical data of rate cycles from 1973 to present day.

Consumer non-cyclicals see the strongest returns after the first rate cut, particularly during recessions, thanks to steady demand for staple goods.

This traditionally defensive sector includes companies such as Procter & Gamble, Walmart, and Coca-Cola. Notably, consumer staples are the only S&P 500 sector that have produced positive returns on average, during the recession stage of the business cycle since 1960. During the slowdown phase, it also outperformed the vast majority of sectors, averaging 15% returns over these periods.

Meanwhile, the tech sector underperforms the market six months after the first rate cut, but performance bounces back over a 12 month period since lower interest rates generally benefit growth stocks by reducing borrowing costs. However, some of today’s largest tech companies have been more resilient to higher rates due to large cash reserves and heightened investor interest in AI-related stocks.

On the other hand, financials historically experience the weakest performance. This is due to the fact that interest rate cuts often signal that the economy is slowing, putting pressure on loan growth, credit losses, and default risk.

To learn more about this topic from a sector-composition perspective, check out this graphic on the largest company in each S&P 500 sector in 2024.