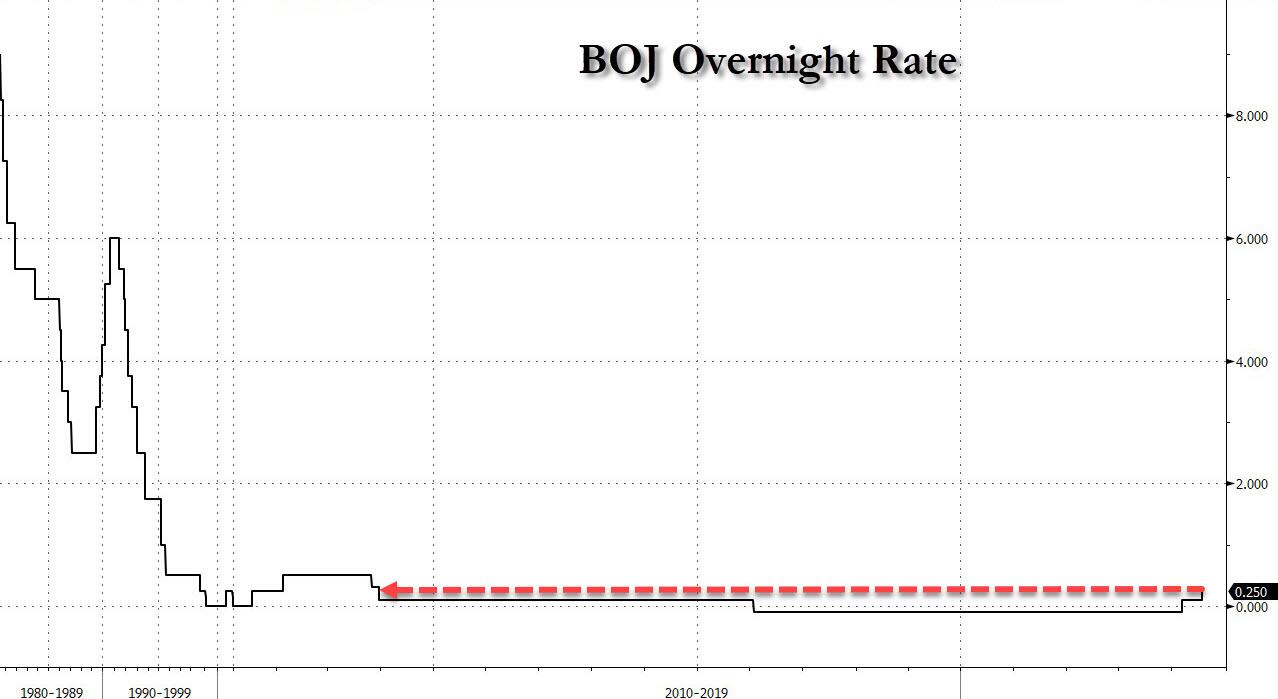

The Bank of Japan has lifted its benchmark interest rate to 0.25% and outlined plans to halve its monthly bond purchases in a decisive, if doomed, move to normalize its monetary policy.

With the Fed and all other central banks either set to move, or already moving rapidly in the opposite direction, the always confused BoJ’s shift to tighter policy will narrow an interest rate gap that has driven record weakness in the yen, marking a big shift for global currency markets. It also comes at a time when Japan's economy is once again slowing, inflation is failing to take hold, wage growth is sputtering.... which is also why this will be the shortest tightening cycle since its last failed attempt to raise rates off the zero lower bound.

The Japanese currency strengthened more than 1% following the decision on Wednesday, sending the USDJPY below 150 against the dollar.

By a majority of 7-2, the BoJ raised its overnight interest rate to “around 0.25 per cent”, the highest level since the global financial crisis in late 2008, from a previous range of 0 to 0.1%. The bank in March ended its negative interest rate policy following decades of on-and-off deflation.

The BoJ also said it would scale back its ¥6tn ($39bn) monthly bond-buying program to about ¥3tn by the spring of 2026, however, it would do so at a much slower pace than many had expected. Specifically, the BOJ said it would cut monthly bond purchases by ¥400 billion every quarter to decrease them to ¥2.9 trillion in 1Q 2026; the market was foreseeing 1 trillion yen per month starting August.

“It’s a hawkish development with the BOJ rate hike, but reduced to some extent by the less-than-expected amount of quantitative tightening,” said Alvin Tan of RBC Capital Markets. “In short, the BOJ decision today does not significantly exceed the hawkish market expectations baked into the meeting.”

Others agreed, Nick Twidale, chief market analyst at ATFX markets said the BOJ's QE taper was "much less than expected and that has hit the yen hard... We’re seeing gapping in a fast moving market, and given the positioning overnight we could see more in the hours ahead."

Today's rate hike came after senior government officials made unusually blunt comments in recent weeks, putting pressure on the BoJ to unwind its ultra-loose monetary policy and arrest the yen’s decline.

At a news conference on Wednesday, central bank governor Kazuo Ueda said the rate decision was made because economic conditions and price movements remained “on track”. But he acknowledged that upside risks to inflation posed by the weaker yen were also a factor.

“We plan to continue raising our policy rate and adjust the degree of monetary accommodation” if economic conditions and inflation move in line with its forecast, Ueda added.

Ahead of the policy decision, traders were evenly split on the prospect of the BoJ lifting short-term interest rates, with some economists cautioning against a move following a string of weak economic data. Core inflation, which excludes volatile food prices, rose 2.6 per cent from a year earlier in June, exceeding the BoJ’s 2 per cent target for 27 consecutive months. However, Japan’s economy contracted in the first three months of the year as the yen’s decline and rising living costs hurt household spending.

“It’s extremely disappointing that the BoJ has chosen to act by ignoring weak economic data. It now looks like it moved to counter the weak yen,” said UBS economist Masamichi Adachi. “The normalisation of Japan’s economy was very precarious to begin with, but the BoJ has made it even more difficult.”

Adachi is spot on, because by caving to government pressure to ease the pressure on the crashing yen - a function of the BOJ's own previous actions - the central bank has only made the next crisis that much worse, which in addition to a brutal stagflationary recession, will also see a bond market crisis, forcing the BOJ to unwind all of its recent actions and then some.

In its forecast, the BOJ said it expected consumer price inflation of 2.1% for the year ended March 2026, instead of the 1.9% it forecast in April. Of course by then the world will be drowning in delfation and Japan will be back to using good old NIRP.

Stefan Angrick, a senior economist at Moody’s Analytics, pointed to the BoJ’s new emphasis on the yen’s inflationary impact but added that the central bank was still “hiking into a weak economy” in the absence of demand-driven inflation.

"I think the BoJ needs to be clear about the fact that they’re changing the rules. They’re not winning the game,” Angrick said. He forecast the next rate increase would be in December, noting that yen pressure on the BoJ was likely to wane once the Fed started cutting rates.

Growing expectations of the BoJ’s rate rise had already boosted the yen against the dollar in the run-up to Wednesday’s meeting. The reversal was aided by government purchases of ¥5.5tn of its own currency earlier this month. The market intervention had the effect of squeezing a substantial volume of short yen positions out of the market, traders said, tamping down the so-called carry trade.

But hedge funds are likely to still have significant short positions in the Japanese currency, so the combination of the BoJ move and a dovish tone by the Fed later on Wednesday could provoke another sharp move higher for the yen, even if it is the last one for a long time.

Yujiro Goto, Nomura’s chief foreign exchange strategist, said the yen’s upward momentum could also be accelerated if Japanese retail investors decide to unwind their large bets on US equities and convert dollar profits back into yen. And judging by the collapse in the USDJPY in recent weeks, that's precisely what is taking place.

And yes, for those who note that it is amusing that it is somehow viewed as hawkish that a 0.15% increase in rates even as the BOJ continues its QE almost full bore (down ¥400 billion from ¥6 trillion), we agree: it is amusing.

The Bank of Japan has lifted its benchmark interest rate to 0.25% and outlined plans to halve its monthly bond purchases in a decisive, if doomed, move to normalize its monetary policy.

With the Fed and all other central banks either set to move, or already moving rapidly in the opposite direction, the always confused BoJ’s shift to tighter policy will narrow an interest rate gap that has driven record weakness in the yen, marking a big shift for global currency markets. It also comes at a time when Japan's economy is once again slowing, inflation is failing to take hold, wage growth is sputtering.... which is also why this will be the shortest tightening cycle since its last failed attempt to raise rates off the zero lower bound.

The Japanese currency strengthened more than 1% following the decision on Wednesday, sending the USDJPY below 150 against the dollar.

By a majority of 7-2, the BoJ raised its overnight interest rate to “around 0.25 per cent”, the highest level since the global financial crisis in late 2008, from a previous range of 0 to 0.1%. The bank in March ended its negative interest rate policy following decades of on-and-off deflation.

The BoJ also said it would scale back its ¥6tn ($39bn) monthly bond-buying program to about ¥3tn by the spring of 2026, however, it would do so at a much slower pace than many had expected. Specifically, the BOJ said it would cut monthly bond purchases by ¥400 billion every quarter to decrease them to ¥2.9 trillion in 1Q 2026; the market was foreseeing 1 trillion yen per month starting August.

“It’s a hawkish development with the BOJ rate hike, but reduced to some extent by the less-than-expected amount of quantitative tightening,” said Alvin Tan of RBC Capital Markets. “In short, the BOJ decision today does not significantly exceed the hawkish market expectations baked into the meeting.”

Others agreed, Nick Twidale, chief market analyst at ATFX markets said the BOJ's QE taper was "much less than expected and that has hit the yen hard... We’re seeing gapping in a fast moving market, and given the positioning overnight we could see more in the hours ahead."

Today's rate hike came after senior government officials made unusually blunt comments in recent weeks, putting pressure on the BoJ to unwind its ultra-loose monetary policy and arrest the yen’s decline.

At a news conference on Wednesday, central bank governor Kazuo Ueda said the rate decision was made because economic conditions and price movements remained “on track”. But he acknowledged that upside risks to inflation posed by the weaker yen were also a factor.

“We plan to continue raising our policy rate and adjust the degree of monetary accommodation” if economic conditions and inflation move in line with its forecast, Ueda added.

Ahead of the policy decision, traders were evenly split on the prospect of the BoJ lifting short-term interest rates, with some economists cautioning against a move following a string of weak economic data. Core inflation, which excludes volatile food prices, rose 2.6 per cent from a year earlier in June, exceeding the BoJ’s 2 per cent target for 27 consecutive months. However, Japan’s economy contracted in the first three months of the year as the yen’s decline and rising living costs hurt household spending.

“It’s extremely disappointing that the BoJ has chosen to act by ignoring weak economic data. It now looks like it moved to counter the weak yen,” said UBS economist Masamichi Adachi. “The normalisation of Japan’s economy was very precarious to begin with, but the BoJ has made it even more difficult.”

Adachi is spot on, because by caving to government pressure to ease the pressure on the crashing yen - a function of the BOJ's own previous actions - the central bank has only made the next crisis that much worse, which in addition to a brutal stagflationary recession, will also see a bond market crisis, forcing the BOJ to unwind all of its recent actions and then some.

In its forecast, the BOJ said it expected consumer price inflation of 2.1% for the year ended March 2026, instead of the 1.9% it forecast in April. Of course by then the world will be drowning in delfation and Japan will be back to using good old NIRP.

Stefan Angrick, a senior economist at Moody’s Analytics, pointed to the BoJ’s new emphasis on the yen’s inflationary impact but added that the central bank was still “hiking into a weak economy” in the absence of demand-driven inflation.

"I think the BoJ needs to be clear about the fact that they’re changing the rules. They’re not winning the game,” Angrick said. He forecast the next rate increase would be in December, noting that yen pressure on the BoJ was likely to wane once the Fed started cutting rates.

Growing expectations of the BoJ’s rate rise had already boosted the yen against the dollar in the run-up to Wednesday’s meeting. The reversal was aided by government purchases of ¥5.5tn of its own currency earlier this month. The market intervention had the effect of squeezing a substantial volume of short yen positions out of the market, traders said, tamping down the so-called carry trade.

But hedge funds are likely to still have significant short positions in the Japanese currency, so the combination of the BoJ move and a dovish tone by the Fed later on Wednesday could provoke another sharp move higher for the yen, even if it is the last one for a long time.

Yujiro Goto, Nomura’s chief foreign exchange strategist, said the yen’s upward momentum could also be accelerated if Japanese retail investors decide to unwind their large bets on US equities and convert dollar profits back into yen. And judging by the collapse in the USDJPY in recent weeks, that's precisely what is taking place.

And yes, for those who note that it is amusing that it is somehow viewed as hawkish that a 0.15% increase in rates even as the BOJ continues its QE almost full bore (down ¥400 billion from ¥6 trillion), we agree: it is amusing.