Almost one thousand points higher and almost a year after he said to short the S&P at 3,900 in December 2022, Mike Wilson - who along with JPM's Marko Kolanovic was the most steadfast bear on Wall Street - has finally capitulated.

Recall that last October, just around the time we and a handful of others said a major market meltup was coming - and it turned out to be the biggest such meltup in history - Morgan Stanley's chief equity strategist Mike Wilson said that his "observations on narrowing breadth, cautious factor leadership, falling earnings revisions and fading consumer and business confidence tell a different story than the consensus, which sees a rally into year-end that's based mostly on bearish sentiment and seasonal tendencies" adding that a "rally into year-end looks more unlikely to us."

In retrospect, "consensus" was right (actually the call for a meltup was anything but consensus, but this is just Mike trying to sound ultra contrarian when in reality he was in the same bearish echo chamber as everyone else in late October), while Wilson's call to kiss a year-end rally goodbye, will go down in history as one of the worst in history...

this may go down as the worst call in history https://t.co/yvljHlo4XR

— zerohedge (@zerohedge) December 1, 2023

... as markets have melted up in a straight line since his note, with a mindblowing 24 weeks of gains since late October, and what's worse Wilson literally bottom-ticked an explosive 30% gain in the S&P since the fateful "no rally" call.

What happened then? Well, having dug himself into an impossibly deep hole, Wilson knew that capitulation would crush his credibility as an analyst who once upon a time was good at timing market inflection points and was hoping that a broken clock would finally be right that stocks would finally crack, and he would be able to go home head held high, writing an "I told you so" note to his clients and readers (even though stocks first moved 20% in the opposite direction of his call, peaking at 4,600 this summer)... if only he could wait a little longer.

And so one week passed, then another, and another, and all through this time Wilson would "explain" why stocks kept levitating higher (i.e., why he was wrong) and instead of flipping his call and joining the momentum higher (and at least saving his clients some money) he would keep doubling down on a losing position... only to "explain" the coming week why, again, stocks kept levitating higher.

Then in late December, Wilson took the first tentative step to admitting he had gotten all of 2023 wrong, when picking up on something we have been pounding the table since last summer, he said that "Equities Have The Green Light To Ramp Higher."

That, however, was about the weakest endorsement of the ongoing melt-up one could muster, and instead of placating his clients and superiors, it only infuriated them further as it was apparent Wilson wanted to have his bearish cake while eating his bullish flip-flop (he refused to change his 4,500 S&P year-end price target), and then in February the humiliation was complete when Wilson - Morgan Stanley's chief US equity strategist - was forced to step down from his role as the chair of the bank's Global Investment Committee, and instead would “focus on serving his key institutional clients, where the demand for generating tactical alpha is intensifying,” which of course was even more hilarious as Wilson had failed to generate any alpha - or beta - since some time in mid-2022.

And so, having pretty much lost everything, both his stock-picking credibility and also his standing in the company's org chart, there was little left for him to lose, which brings us to today when in his just published "mid-year outlook" note (available to pro subscribers in the usual place), Wilson - formerly one of Wall Street’s most prominent bears - just turned positive in his outlook for US stocks.

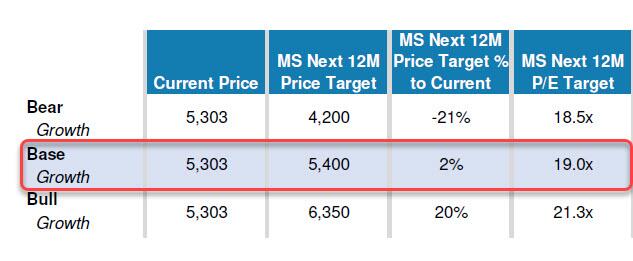

That's right: having missed the most powerful rally in a generation, with the S&P and Nasdaq trading at all time highs, and the Dow above 40,000 for the first time ever, Wilson "stunned" his readers by dramatically raising his June 2025 S&P price target to 5,400, from his previous forecast which saw the S&P tumbling to 4,500, or 15%, by December.

Hoping to put his entire bearish phase behind him, Wilson jumps straight to declaring that in his latest "base case 12-month price target moves to 5,400" and explains that "In the base case, we forecast a 19x P/E multiple on 12-month forward EPS (June 2026) of US$283, which equates to a 5,400 forward 12-month price target. Our 2024 and 2025 earnings growth forecasts (8% and 13%, respectively) assume healthy, mid single- digit top-line growth in addition to margin expansion in both years as positive operating leverage resumes (particularly in 2025)." Funny how he did not "assume" any of these things as recently as a week ago.

And while Wilson wistfully contemplates his bear case that could see stocks drop to 4,200 (or roughly what was his base case On this front, he also notes that his bull (6,350) case represents ~20% upside potential versus the current index level, respectively: "Our bull case reflects stronger (11-15%) EPS growth driven by continued fiscal support and cyclical/structural drivers out to 2026 alongside multiple expansion to ~21x. Our bear case incorporates a recession (negative EPS growth and multiple compression)."

There is a bunch of other arguments for the various bear and bull cases (all laid out in detail in his note available to pro subs), but the bottom line is that Wilson finally admits he really has no idea what is coming (hence the 20% upside, downside interval of "confidence") but he knows that whatever he predicted before is wrong.

Amusingly, even in his capitulation, he desperately tries to hold on to the bearish case as if that - or his reputation - even matters any more. To do that, he converts all nominal numbers into inflation adjusted ones or, even better, shows returns in gold terms, something we haven't seen since the days of Dennis Gartman:

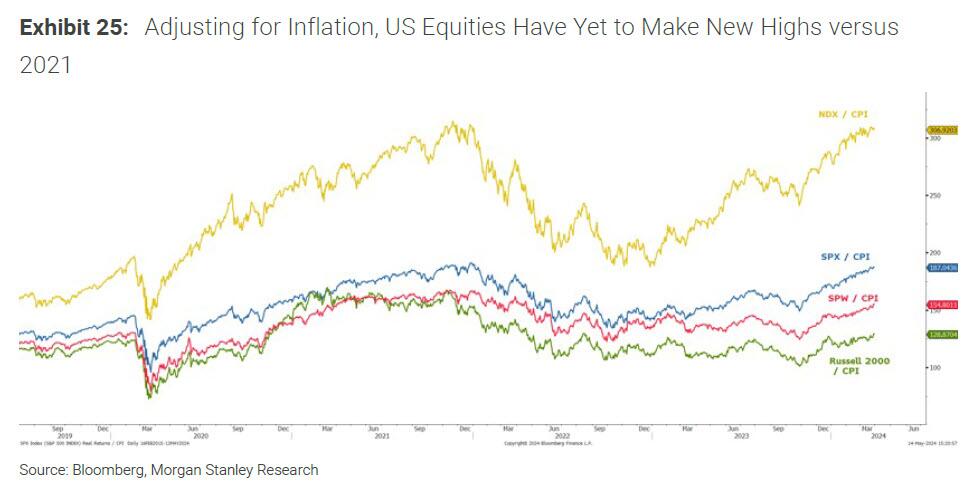

Finally, real equity returns have looked less attractive over the past few years as policy makers try to inflate out of the excessive debt the government and creditors have accumulated over the past 2 decades. More specifically, when looking at equity returns after inflation, we have yet to make new highs in all of the major indices. In a world where returns are measured and rewarded in nominal terms, such an analysis may not be relevant to most clients. However, we do think there is an important message in this analysis as a sign that this rally is not nearly as strong as the one in 2020-21 when companies were able to extract price and margin more easily. In short, it could be telling us something about the health of the real economy and sustainability of profits and margins.

When we look at real returns using the price of gold, the performance results are weaker. We think this ratio captures much of what has been going on since the pandemic, including the intent of policy. First, notice that the real returns in gold were exceptionally strong coming out of the COVID lows in March 2020. This very much syncs with our view at the time that there would be significant operating leverage and real earnings growth as companies were able to extract pricing while simultaneously keeping costs under control during the lock downs. This was by far the best time to be fully invested (i.e., April 2020-November 2021) across a wide swath of the market. Since then, it’s been much more challenging and narrow as most companies have struggled to maintain the extraordinary margins and over-earning enjoyed during the pandemic. With the rally since last October due largely to multiple expansion, investors should be asking themselves if this rise in valuations is justified. We don't think it is which is why we still have multiples coming down moderately in our base case view which assumes a soft/goldilocks landing for the economy and strong earnings growth. In the bear case context, we worry that if the soft landing outcome doesn’t happen, the multiple contraction will be swift as investors realize the performance dynamic in nominal returns is about to reverse. The breakdown in equity markets when shown in gold terms is an early warning sign that perhaps the late cycle environment may be at greater risk than appreciated.

Yes, Mike, the risk is far "greater" than appreciated, but this is it for you: you have capitulated and you don't get to say "told you so... in the small print" when stocks crash, which they will now that the last bears have thrown in the towel, just as we predicted back in February 2023 when we said that the "rally won't end until Wilson and Marko turn bullish."

Rally won't end until Wilson and Marko turn bullish

— zerohedge (@zerohedge) February 7, 2023

And yet, despite Wilson's capitulation, the bulls - and the rally - are not dead just yet: that's because only one half of our forecast has materialized. Yes, Wilson finally flipped, but in a desperate attempt to keep the rally going, even as his trading desk beats the bullish drum day after day, JPMorgan's equivalent to Wilson, Marko Kolanovic, just published a note (also available to pro subs) - as if desperate to respond to the U-turn just taken by his Morgan Stanley colleague - in which he reiterated his bearish view, urging them not to buy stocks, while acknowledging that this negative outlook has hurt JPMorgan’s model portfolio allocation over the past year as global equity markets rose to record highs. As Bloomberg notes, "he cited a litany of reasons for maintaining his pessimistic position, including high valuations, the likelihood rates will remain restrictive for longer, elevated inflation readings, consumer stress, and geopolitical uncertainty."

Of course, none of these are in any way unknown or not priced in, so the Croat hasn't said anything the market doesn't already know, and if anything he merely continues to feed the extremely bullish JPM flow trading desk with what little sales JPM's retail clients have left.

“A negative stance on equities has hurt the performance of our multi-asset portfolio over the past year,” Marko acknowledged, while adding, “we do not see equities as attractive investments at the moment and we don’t see a reason to change our stance.”

Kolanovic has the lowest year-end target for the S&P 500 at 4,200, implying a drop of more than 20% from Monday’s closing level.

Yet what remains extremely laughable, if not outright criminal, is that at the same time that Kolanovic pounds the table on his ridiculous bearish view that has cost anyone who listened to him the 50% gain in the S&P since Oct 2022 when Marko turned bearish, the JPM trading desk could not be more bullish. Here is what JPM market intel trader Andrew Tyler wrote this morning in the bank's daily note to a select number of institutional clients:

Tactically Bullish. Still following the formula of (i) at/above average GDP growth plus (ii) positive earnings growth and a (iii) paused Fed translate to a bull market. When considering the macro component, there is a clear slowing of the economy, but I remain less concerned about that then some clients. Why? I think survey data and diffusion indices (ISM/PMI) are painting a picture that is more dire than hard data, earnings, and consumer behavior suggest. For example, ISM-Mfg has had one expansionary print since October 2022; historically, one would conclude that the US was in a recession but instead we saw real GDP print above the long-term trend in 6 of the last 7 quarters. More generally, I think we are still normalizing to pre-COVID times and not seeing a material deterioration from there. While there is a divergence in Consumer outcomes based on income, I think the aggregate consumer remains in good shape. (more in the full JPM note available to pro subs).

So yes, the meltup will continue because while Wilson has had enough of being "contrarian", Marko still hopes to find a few remaining holdouts who i) still bother to read what he writes and ii) will sell what risk assets they have to, who else, JPMorgan.

More in the full note from Morgan Stanley and JPMorgan.

Almost one thousand points higher and almost a year after he said to short the S&P at 3,900 in December 2022, Mike Wilson - who along with JPM's Marko Kolanovic was the most steadfast bear on Wall Street - has finally capitulated.

Recall that last October, just around the time we and a handful of others said a major market meltup was coming - and it turned out to be the biggest such meltup in history - Morgan Stanley's chief equity strategist Mike Wilson said that his "observations on narrowing breadth, cautious factor leadership, falling earnings revisions and fading consumer and business confidence tell a different story than the consensus, which sees a rally into year-end that's based mostly on bearish sentiment and seasonal tendencies" adding that a "rally into year-end looks more unlikely to us."

In retrospect, "consensus" was right (actually the call for a meltup was anything but consensus, but this is just Mike trying to sound ultra contrarian when in reality he was in the same bearish echo chamber as everyone else in late October), while Wilson's call to kiss a year-end rally goodbye, will go down in history as one of the worst in history...

this may go down as the worst call in history https://t.co/yvljHlo4XR

— zerohedge (@zerohedge) December 1, 2023

... as markets have melted up in a straight line since his note, with a mindblowing 24 weeks of gains since late October, and what's worse Wilson literally bottom-ticked an explosive 30% gain in the S&P since the fateful "no rally" call.

What happened then? Well, having dug himself into an impossibly deep hole, Wilson knew that capitulation would crush his credibility as an analyst who once upon a time was good at timing market inflection points and was hoping that a broken clock would finally be right that stocks would finally crack, and he would be able to go home head held high, writing an "I told you so" note to his clients and readers (even though stocks first moved 20% in the opposite direction of his call, peaking at 4,600 this summer)... if only he could wait a little longer.

And so one week passed, then another, and another, and all through this time Wilson would "explain" why stocks kept levitating higher (i.e., why he was wrong) and instead of flipping his call and joining the momentum higher (and at least saving his clients some money) he would keep doubling down on a losing position... only to "explain" the coming week why, again, stocks kept levitating higher.

Then in late December, Wilson took the first tentative step to admitting he had gotten all of 2023 wrong, when picking up on something we have been pounding the table since last summer, he said that "Equities Have The Green Light To Ramp Higher."

That, however, was about the weakest endorsement of the ongoing melt-up one could muster, and instead of placating his clients and superiors, it only infuriated them further as it was apparent Wilson wanted to have his bearish cake while eating his bullish flip-flop (he refused to change his 4,500 S&P year-end price target), and then in February the humiliation was complete when Wilson - Morgan Stanley's chief US equity strategist - was forced to step down from his role as the chair of the bank's Global Investment Committee, and instead would “focus on serving his key institutional clients, where the demand for generating tactical alpha is intensifying,” which of course was even more hilarious as Wilson had failed to generate any alpha - or beta - since some time in mid-2022.

And so, having pretty much lost everything, both his stock-picking credibility and also his standing in the company's org chart, there was little left for him to lose, which brings us to today when in his just published "mid-year outlook" note (available to pro subscribers in the usual place), Wilson - formerly one of Wall Street’s most prominent bears - just turned positive in his outlook for US stocks.

That's right: having missed the most powerful rally in a generation, with the S&P and Nasdaq trading at all time highs, and the Dow above 40,000 for the first time ever, Wilson "stunned" his readers by dramatically raising his June 2025 S&P price target to 5,400, from his previous forecast which saw the S&P tumbling to 4,500, or 15%, by December.

Hoping to put his entire bearish phase behind him, Wilson jumps straight to declaring that in his latest "base case 12-month price target moves to 5,400" and explains that "In the base case, we forecast a 19x P/E multiple on 12-month forward EPS (June 2026) of US$283, which equates to a 5,400 forward 12-month price target. Our 2024 and 2025 earnings growth forecasts (8% and 13%, respectively) assume healthy, mid single- digit top-line growth in addition to margin expansion in both years as positive operating leverage resumes (particularly in 2025)." Funny how he did not "assume" any of these things as recently as a week ago.

And while Wilson wistfully contemplates his bear case that could see stocks drop to 4,200 (or roughly what was his base case On this front, he also notes that his bull (6,350) case represents ~20% upside potential versus the current index level, respectively: "Our bull case reflects stronger (11-15%) EPS growth driven by continued fiscal support and cyclical/structural drivers out to 2026 alongside multiple expansion to ~21x. Our bear case incorporates a recession (negative EPS growth and multiple compression)."

There is a bunch of other arguments for the various bear and bull cases (all laid out in detail in his note available to pro subs), but the bottom line is that Wilson finally admits he really has no idea what is coming (hence the 20% upside, downside interval of "confidence") but he knows that whatever he predicted before is wrong.

Amusingly, even in his capitulation, he desperately tries to hold on to the bearish case as if that - or his reputation - even matters any more. To do that, he converts all nominal numbers into inflation adjusted ones or, even better, shows returns in gold terms, something we haven't seen since the days of Dennis Gartman:

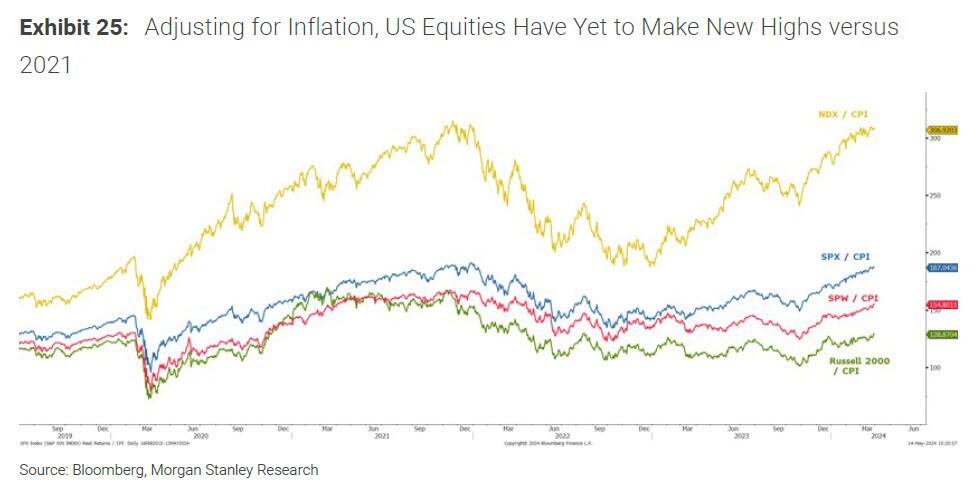

Finally, real equity returns have looked less attractive over the past few years as policy makers try to inflate out of the excessive debt the government and creditors have accumulated over the past 2 decades. More specifically, when looking at equity returns after inflation, we have yet to make new highs in all of the major indices. In a world where returns are measured and rewarded in nominal terms, such an analysis may not be relevant to most clients. However, we do think there is an important message in this analysis as a sign that this rally is not nearly as strong as the one in 2020-21 when companies were able to extract price and margin more easily. In short, it could be telling us something about the health of the real economy and sustainability of profits and margins.

When we look at real returns using the price of gold, the performance results are weaker. We think this ratio captures much of what has been going on since the pandemic, including the intent of policy. First, notice that the real returns in gold were exceptionally strong coming out of the COVID lows in March 2020. This very much syncs with our view at the time that there would be significant operating leverage and real earnings growth as companies were able to extract pricing while simultaneously keeping costs under control during the lock downs. This was by far the best time to be fully invested (i.e., April 2020-November 2021) across a wide swath of the market. Since then, it’s been much more challenging and narrow as most companies have struggled to maintain the extraordinary margins and over-earning enjoyed during the pandemic. With the rally since last October due largely to multiple expansion, investors should be asking themselves if this rise in valuations is justified. We don't think it is which is why we still have multiples coming down moderately in our base case view which assumes a soft/goldilocks landing for the economy and strong earnings growth. In the bear case context, we worry that if the soft landing outcome doesn’t happen, the multiple contraction will be swift as investors realize the performance dynamic in nominal returns is about to reverse. The breakdown in equity markets when shown in gold terms is an early warning sign that perhaps the late cycle environment may be at greater risk than appreciated.

Yes, Mike, the risk is far "greater" than appreciated, but this is it for you: you have capitulated and you don't get to say "told you so... in the small print" when stocks crash, which they will now that the last bears have thrown in the towel, just as we predicted back in February 2023 when we said that the "rally won't end until Wilson and Marko turn bullish."

Rally won't end until Wilson and Marko turn bullish

— zerohedge (@zerohedge) February 7, 2023

And yet, despite Wilson's capitulation, the bulls - and the rally - are not dead just yet: that's because only one half of our forecast has materialized. Yes, Wilson finally flipped, but in a desperate attempt to keep the rally going, even as his trading desk beats the bullish drum day after day, JPMorgan's equivalent to Wilson, Marko Kolanovic, just published a note (also available to pro subs) - as if desperate to respond to the U-turn just taken by his Morgan Stanley colleague - in which he reiterated his bearish view, urging them not to buy stocks, while acknowledging that this negative outlook has hurt JPMorgan’s model portfolio allocation over the past year as global equity markets rose to record highs. As Bloomberg notes, "he cited a litany of reasons for maintaining his pessimistic position, including high valuations, the likelihood rates will remain restrictive for longer, elevated inflation readings, consumer stress, and geopolitical uncertainty."

Of course, none of these are in any way unknown or not priced in, so the Croat hasn't said anything the market doesn't already know, and if anything he merely continues to feed the extremely bullish JPM flow trading desk with what little sales JPM's retail clients have left.

“A negative stance on equities has hurt the performance of our multi-asset portfolio over the past year,” Marko acknowledged, while adding, “we do not see equities as attractive investments at the moment and we don’t see a reason to change our stance.”

Kolanovic has the lowest year-end target for the S&P 500 at 4,200, implying a drop of more than 20% from Monday’s closing level.

Yet what remains extremely laughable, if not outright criminal, is that at the same time that Kolanovic pounds the table on his ridiculous bearish view that has cost anyone who listened to him the 50% gain in the S&P since Oct 2022 when Marko turned bearish, the JPM trading desk could not be more bullish. Here is what JPM market intel trader Andrew Tyler wrote this morning in the bank's daily note to a select number of institutional clients:

Tactically Bullish. Still following the formula of (i) at/above average GDP growth plus (ii) positive earnings growth and a (iii) paused Fed translate to a bull market. When considering the macro component, there is a clear slowing of the economy, but I remain less concerned about that then some clients. Why? I think survey data and diffusion indices (ISM/PMI) are painting a picture that is more dire than hard data, earnings, and consumer behavior suggest. For example, ISM-Mfg has had one expansionary print since October 2022; historically, one would conclude that the US was in a recession but instead we saw real GDP print above the long-term trend in 6 of the last 7 quarters. More generally, I think we are still normalizing to pre-COVID times and not seeing a material deterioration from there. While there is a divergence in Consumer outcomes based on income, I think the aggregate consumer remains in good shape. (more in the full JPM note available to pro subs).

So yes, the meltup will continue because while Wilson has had enough of being "contrarian", Marko still hopes to find a few remaining holdouts who i) still bother to read what he writes and ii) will sell what risk assets they have to, who else, JPMorgan.

More in the full note from Morgan Stanley and JPMorgan.