A bear market in the used car market was confirmed in November and has since worsened through April. At the same time, negative equity values are hitting new record highs while auto insurance rates have soared the most since the mid-1970s. While gas prices at the pump are elevated, the environment to operate a vehicle is probably one of the worst ever. Just listen to Gen-Z and millennial users on X bitch and moan about $1,000 monthly car payments and other absurd costs associated with driving.

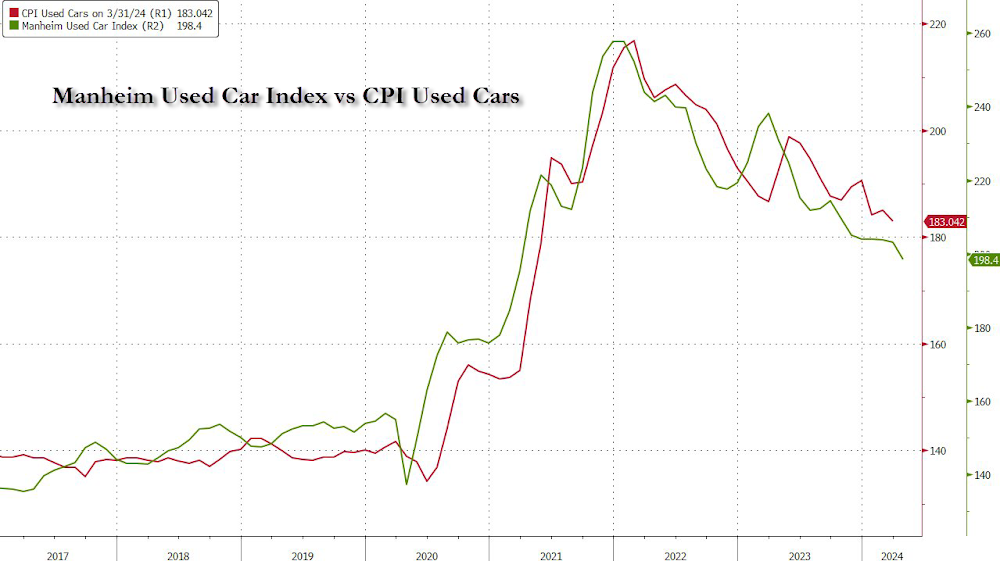

The Manheim Used Vehicle Value Index fell to 198.4 in April, a 14% drop from one year ago. This is the index's lowest print since the first quarter of 2021. As for the bear market, the index is down 23% from the high and quickly falling - there could be air pockets given the rapid upward moves three years ago - and that demand has been suppressed given a high-interest rate environment.

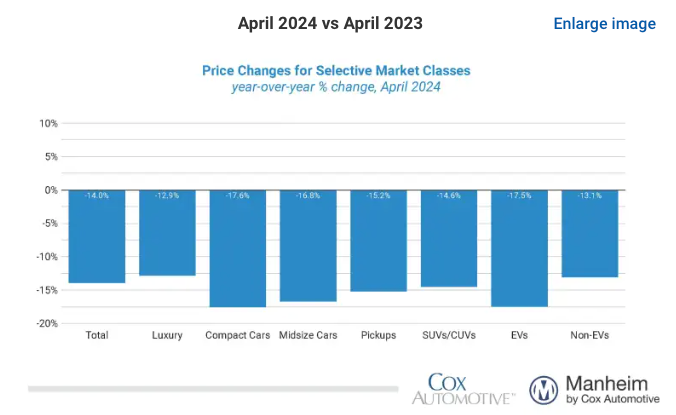

All vehicle segments of the Manheim Used Vehicle Value Index experienced seasonally adjusted prices that were down double digits year over year in April. Luxury was the only segment that was not hit the hardest, down just 12.9%. The worst-performing segment was compact cars, down 17.6% compared with last year, followed by midsize cars, down 16.8%, and pickups, down 15.2%. EVs were down 17.5%.

This is a significant worry for millions of Americans who bought cars during the pandemic mania, which basically involved spending free money provided by the Federal Reserve, only now discovering that their loans are plunging into underwater territory.

According to a recent Edmunds note, 20% of new vehicle sales involving a trade-in had negative equity during the October-through-December period—the highest level since 2021.

Negative equity values soared to a new record high of $6,064 during the period, a massive 46% increase from late 2021.

We warned readers in 2023 about the worsening negative equity situation for heavily indebted drivers:

- Negative Equity Surges: More Consumers Find Themselves In Underwater Auto Loans

- Number Of Americans In Upside-Down Auto Loans Continues To Worsen

Adding to the financial stress for drivers, there's also the concern that Joe Biden's sticky inflation continues to send auto insurance rates to the highest levels since the inflation shitstorm in the mid-1970s.

We've pointed out that ridiculous repair bills for newer vehicles (cough, cough, EVs) are likely the main reason rates are higher.

- Rivian Owner Shocked By $41,000 Repair Bill For Minor Damage

- "Shocking Number": Rivian Owner Sees $42,000 Repair Bill For Minor Accident

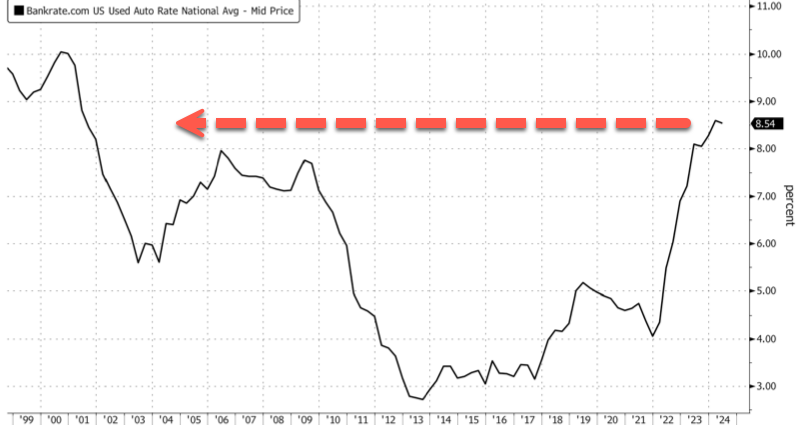

Right now, drivers are paralyzed as the average used car auto loans tracked by Bankrate surged again - now exceeding 8.5%.

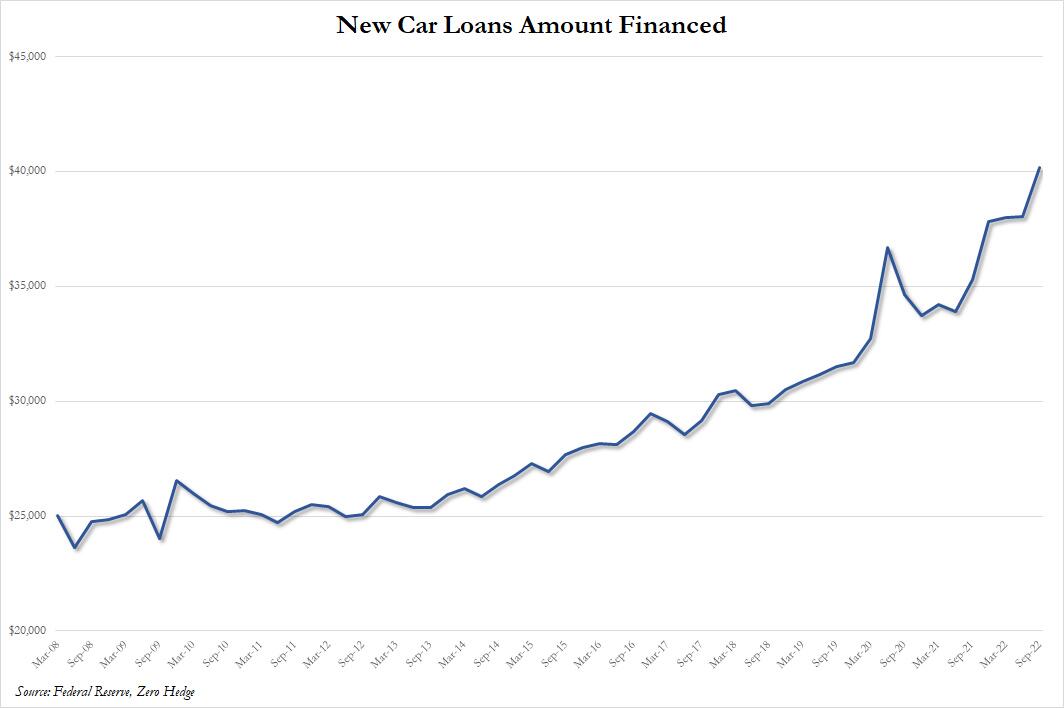

The average new car loan has reached a record high of $40,000.

In recent months, Joseph Yoon, consumer insights analyst for Edmunds, told Bloomberg:

"We're in this situation where combined with the cost of the vehicles being so high and the interest rates being so historically high, you have a lot of people who are in bad car loans."

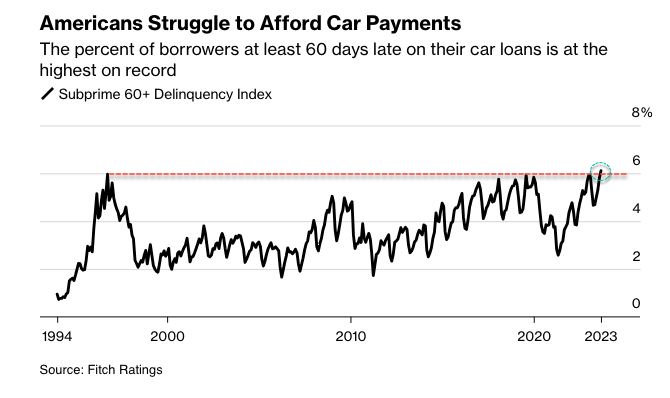

To Yoon's point, the percentage of subprime auto borrowers at least 60 days past due in September topped 6.11%, the highest ever.

Out of all this gloom and doom for drivers. There's good news on the inflation front: falling Manheim used car prices will only result in a lower future print for the US CPI Used Car index.

So the big question is when will the bear market in used car prices bottom?

Car owners should certaily not be looking for any bailouts from The Fed anytime soon (or Biden, who is too busy paying off student loans). Higher rates and longer is the theme, no matter the jawboning, with less than two cuts now priced in for the whole of 2024 (down from over seven at the start of the year).

A bear market in the used car market was confirmed in November and has since worsened through April. At the same time, negative equity values are hitting new record highs while auto insurance rates have soared the most since the mid-1970s. While gas prices at the pump are elevated, the environment to operate a vehicle is probably one of the worst ever. Just listen to Gen-Z and millennial users on X bitch and moan about $1,000 monthly car payments and other absurd costs associated with driving.

The Manheim Used Vehicle Value Index fell to 198.4 in April, a 14% drop from one year ago. This is the index's lowest print since the first quarter of 2021. As for the bear market, the index is down 23% from the high and quickly falling - there could be air pockets given the rapid upward moves three years ago - and that demand has been suppressed given a high-interest rate environment.

All vehicle segments of the Manheim Used Vehicle Value Index experienced seasonally adjusted prices that were down double digits year over year in April. Luxury was the only segment that was not hit the hardest, down just 12.9%. The worst-performing segment was compact cars, down 17.6% compared with last year, followed by midsize cars, down 16.8%, and pickups, down 15.2%. EVs were down 17.5%.

This is a significant worry for millions of Americans who bought cars during the pandemic mania, which basically involved spending free money provided by the Federal Reserve, only now discovering that their loans are plunging into underwater territory.

According to a recent Edmunds note, 20% of new vehicle sales involving a trade-in had negative equity during the October-through-December period—the highest level since 2021.

Negative equity values soared to a new record high of $6,064 during the period, a massive 46% increase from late 2021.

We warned readers in 2023 about the worsening negative equity situation for heavily indebted drivers:

- Negative Equity Surges: More Consumers Find Themselves In Underwater Auto Loans

- Number Of Americans In Upside-Down Auto Loans Continues To Worsen

Adding to the financial stress for drivers, there's also the concern that Joe Biden's sticky inflation continues to send auto insurance rates to the highest levels since the inflation shitstorm in the mid-1970s.

We've pointed out that ridiculous repair bills for newer vehicles (cough, cough, EVs) are likely the main reason rates are higher.

- Rivian Owner Shocked By $41,000 Repair Bill For Minor Damage

- "Shocking Number": Rivian Owner Sees $42,000 Repair Bill For Minor Accident

Right now, drivers are paralyzed as the average used car auto loans tracked by Bankrate surged again - now exceeding 8.5%.

The average new car loan has reached a record high of $40,000.

In recent months, Joseph Yoon, consumer insights analyst for Edmunds, told Bloomberg:

"We're in this situation where combined with the cost of the vehicles being so high and the interest rates being so historically high, you have a lot of people who are in bad car loans."

To Yoon's point, the percentage of subprime auto borrowers at least 60 days past due in September topped 6.11%, the highest ever.

Out of all this gloom and doom for drivers. There's good news on the inflation front: falling Manheim used car prices will only result in a lower future print for the US CPI Used Car index.

So the big question is when will the bear market in used car prices bottom?

Car owners should certaily not be looking for any bailouts from The Fed anytime soon (or Biden, who is too busy paying off student loans). Higher rates and longer is the theme, no matter the jawboning, with less than two cuts now priced in for the whole of 2024 (down from over seven at the start of the year).